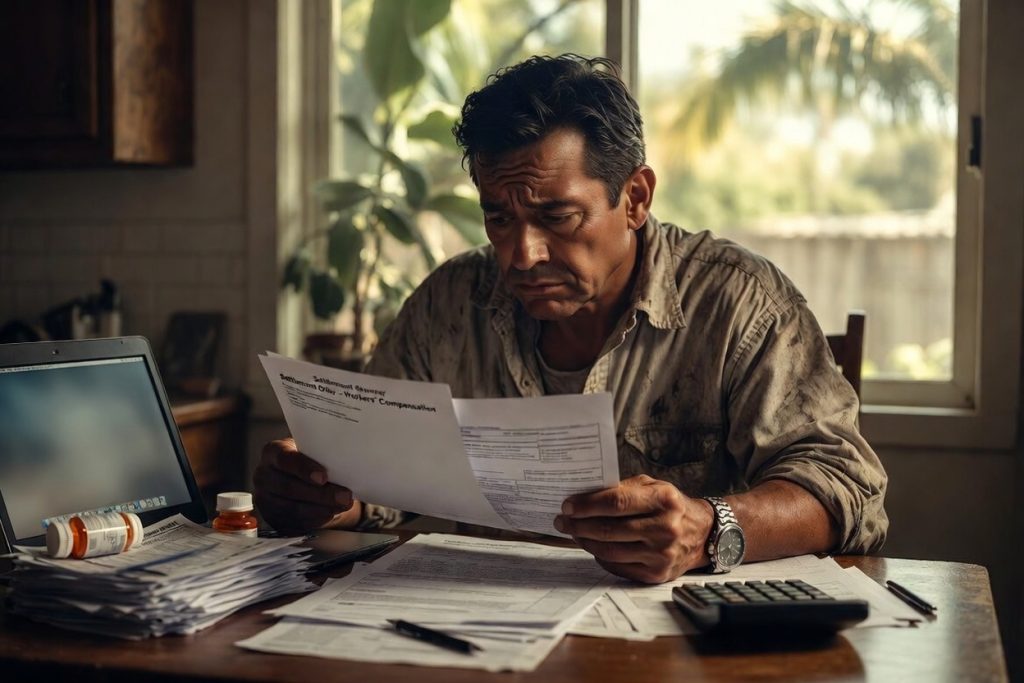

If you have been injured on the job in California and the insurance company just sent you a settlement offer, you are probably staring at the number wondering one thing: Should I take it?

You are not alone. Thousands of injured workers across Orange County, Los Angeles, San Diego, and Riverside ask this exact question every year, especially now in 2026, when medical costs are rising, benefit rates have adjusted with the State Average Weekly Wage, and new worker-protection laws emphasize fair treatment. The pressure is real: bills are piling up, your body hurts, and the claims adjuster is calling, saying this is our best offer or take it or we will drag this out.

Here is the straight truth most insurance companies hope you never hear: the first workers’ comp settlement offer in California is almost never the best offer. In fact, data and real case results show first offers are routinely 30 to 50 percent lower than what an experienced attorney can negotiate. Accepting it too early can cost you tens or even hundreds of thousands of dollars in future medical care, lost wages, and permanent disability benefits.

At Laguna Law Firm, we have been fighting for injured workers in California since 2008. Our attorneys have turned 12,000 dollar first offers into 152,000 dollar settlements and 18,000 dollar lowballs into 195,000 dollar-plus recoveries with open future medical care. This 2026 guide will walk you through exactly what to do when that first offer lands in your inbox, so you can make the smartest decision for your health, your family, and your future.

Understanding Workers’ Compensation Settlements in California

California’s workers’ compensation system is a no-fault insurance program designed to provide medical treatment, temporary disability pay, and permanent disability benefits when you are hurt at work. Once your claim is accepted (or presumed accepted after 90 days under current rules), the insurance company eventually makes a settlement offer, usually after you reach maximum medical improvement (MMI), the point doctors say your condition will not improve much more with treatment.

Settlements are not random. They are calculated based on:

- Your permanent disability (PD) rating (using the AMA Guides and California’s rating schedule)

- Future medical needs

- Lost earning capacity

- Any liens (Medicare, Medi-Cal, etc.)

- Vocational rehabilitation or job retraining

The two primary ways cases close in California are Stipulated Award (Stips) and Compromise and Release (C&R). Knowing the difference is critical before you sign anything.

C&R vs. Stipulated Award: Which Settlement Type Is Right for You in 2026?

| Feature | Stipulated Award (Stips) | Compromise and Release (C&R) |

|---|---|---|

| Payment Structure | Bi-weekly checks over weeks/months/years | One-time lump-sum check |

| Future Medical Care | Remains open for life (insurance pays approved treatment) | Closed permanently (you pay out of pocket) |

| Permanent Disability | Paid at the rated percentage | Can be negotiated higher because medical is closed |

| Flexibility | Can reopen for worsening condition (5-year rule) | Final and binding, no going back |

| Best For | Serious injuries needing ongoing care (back surgery, chronic pain) | Workers who want cash now and can manage care privately |

| Typical Negotiation Potential | Moderate | High (insurance pays extra to close medical) |

Most first offers come as a C&R because insurance companies love closing files forever. But if you still need surgery, injections, physical therapy, or pain management in 2026 and beyond, signing a C&R without proper valuation could leave you financially devastated when those bills arrive.

Why the First Workers’ Comp Settlement Offer Is Almost Always Too Low

Insurance adjusters are trained to minimize payouts. Their first offer is a starting point in a negotiation poker game, designed to test whether you will fold early. Common tactics include:

- Lowballing your PD rating (for example, claiming 5 percent when medical evidence supports 25 to 40 percent)

- Ignoring future medical costs

- Downplaying lost earning capacity if you cannot return to your old job

- Pressuring you while you are still in pain or out of work

Recent analyses show first offers often undervalue cases by 40 percent or more compared to final settlements handled by attorneys. Why? Because without legal representation, most workers do not have access to Qualified Medical Evaluators (QMEs), independent rating calculations, or lien negotiation expertise.

The Real Risks of Accepting the First Offer in California

- You close the door on future medical care forever. With medical inflation and new treatment options in 2026 (advanced spinal injections, regenerative therapies), what seems covered today may not be enough tomorrow.

- You undervalue your permanent disability. A few percentage points on your PD rating can mean thousands of dollars per week in benefits.

- You lose leverage for liens and Medicare set-asides. Attorneys routinely negotiate liens down, sometimes to zero, putting more money in your pocket.

- You risk financial instability. A lump-sum that looks decent today can disappear fast if you need ongoing treatment or cannot work at full capacity.

- You waive rights to appeal or reopen. Once approved by a workers’ comp judge, the deal is usually final.

Real talk: We have seen clients regret accepting first offers when their condition worsened six months later and they had no insurance coverage left for care.

When Might It Actually Make Sense to Accept the First Offer? (Rare Cases)

There are exceptions, but they are uncommon:

- Your injury is minor, fully healed, no future treatment needed, and the offer covers all lost wages plus a fair PD rating.

- You have already consulted an attorney who ran the numbers and confirmed it is full value.

- You need immediate cash for a specific reason (mortgage, family emergency) and understand the trade-offs.

Even then, have a California workers’ comp lawyer review it first. The consultation is free and could save you thousands.

How to Evaluate If the Offer Is Fair – 2026 Checklist

Before you accept or reject:

- Has your doctor declared you Permanent and Stationary (P&S)?

- Did you receive a proper PD rating under current California guidelines?

- Are future medical costs (surgeries, meds, therapy) fully accounted for?

- Have all liens been negotiated?

- Does the offer reflect your true wage loss and vocational impact?

- Have benefit rates been updated for 2026 (higher TD/PD max rates tied to SAWW)?

If you cannot answer yes to everything, the offer is probably low.

The Power of Having a California Workers’ Comp Lawyer on Your Side

Here is what changes when Laguna Law Firm steps in:

- We obtain strong medical evidence and request QME/AME evaluations to push your PD rating higher.

- We calculate exact future medical needs using current 2026 cost data.

- We negotiate liens aggressively (Medicare/Medi-Cal often reduced dramatically).

- We know exactly when to counter-offer and how high to push, because we have done it thousands of times.

- No upfront fees. Our fee (typically 15 percent) comes only from the increased settlement we win for you.

Real Results from Laguna Law Firm Clients (2025 to 2026 Cases)

- Warehouse worker, herniated disc: Insurance first offer 12,000 dollars. After proper rating and negotiation: 152,000 dollars.

- Construction worker, back injury: First offer 18,000 dollars. Final settlement: 195,000 dollars plus lifetime medical care.

- Nurse with repetitive stress injuries: Claim initially denied. After appeal and negotiation: 285,000 dollars plus lifetime medical.

- Delivery driver, truck accident: Combined workers’ comp plus third-party recovery: 1.2 million dollars total.

These are not hypotheticals. They are the kind of results our Mission Viejo-based team delivers every month for clients throughout Southern California.

2026 California Workers’ Comp Updates Every Injured Worker Should Know

New laws effective January 1, 2026 strengthen worker protections, including better tools against employer fraud in providing coverage (SB 847) and the Workplace Know Your Rights Act requiring annual notices about your workers’ comp rights. Claims are being evaluated earlier and more aggressively by insurers, making documentation and prompt legal help more important than ever. Benefit rates have increased with the State Average Weekly Wage, and average settlements for serious injuries (head/spine) now commonly exceed 90,000 dollars when handled properly.

Frequently Asked Questions About First Workers’ Comp Settlement Offers in California

Should I accept the first workers’ comp settlement offer in California? Almost never. The first offer is a lowball starting point. Rejecting it and negotiating (or hiring an attorney) routinely increases the final payout significantly.

How long do I have to accept or reject a workers’ comp offer in California? There is no strict deadline, but do not delay too long. Insurers may withdraw or reduce it. Take at least 48 to 72 hours and consult an attorney immediately.

What is the average workers’ comp settlement in California in 2026? It varies widely by injury. Minor claims may settle for 20,000 to 50,000 dollars; back/spine injuries often 60,000 to 200,000 dollars plus; head/brain injuries average around 90,000 to 500,000 dollars plus when future care is properly valued.

Can I negotiate my workers’ comp settlement offer myself? You can, but most workers leave significant money on the table. Attorneys know the rating schedules, medical evidence standards, and insurer tactics that self-represented workers do not.

Does hiring a lawyer cost me anything upfront? No. California workers’ comp attorneys work on contingency. You pay nothing unless we increase your settlement.

Ready to Get the Settlement You Actually Deserve?

Do not let the insurance company decide your future. If you have received a first (or any) workers’ comp settlement offer in California, call Laguna Law Firm today at (949) 930-1386 for a free, no-obligation case review. We will evaluate your offer, explain your options in plain English, and fight to maximize every benefit you are entitled to, whether that is a higher lump-sum C&R or a Stipulated Award with open medical care.

You have already done the hardest part by getting injured at work. Let us handle the rest.

Laguna Law Firm Serving injured workers throughout Orange County, Los Angeles, San Diego, Riverside and statewide Phone: (949) 930-1386 Website: lagunalawfirm.com Se habla espanol. 24/7 availability. Free consultations